Introduction

Below is a look at some notable survey results from 2025.

For anyone unfamiliar, these survey questions come from the @garagegymexperiment Instagram account. I’ve been running these surveys for about 7 years now. Nevertheless, most of the survey figures do not shift dramatically from year to year, and I feel it is statistically significant.

Many companies have told me these survey results have given them many ideas and helped them direct their efforts as they look to develop new products.

If you have any questions or would like to discuss, please email me at jake@garagegymexperiment.com.

I’ve also ran through these numbers in video/audio form, you can watch/listen to on YouTube, Spotify, Apple, or wherever you listen to podcasts.

Who is Answering These Questions?

It’s important to keep in mind who is answering these survey questions. These respondents represent some of the most passionate and engaged home gym owners in the community. They are often the ones setting the tone for where the home gym industry is headed and helping guide companies on what serious home gym owners actually want.

These are the people quietly pushing the industry forward every day. They’re usually the first to try new equipment, stress-test it in real training, and share honest feedback—good or bad. That feedback shows up across multiple forums like Reddit, Discord servers, Facebook groups, Instagram, YouTube comments, and podcasts—places where brands are actively listening.

They also shape demand. When this group starts prioritizing space efficiency, modular systems, better ergonomics, or higher build quality, companies adjust. Many of today’s product ecosystems and refinements can be traced back to conversations these owners were having years ago.

Just as important, they help educate the rest of the community—showing newer lifters what’s worth buying, what isn’t, and how to train effectively at home. That raises the standard across the entire market.

They’re not just consumers—they’re the filter that helps decide where the home gym industry goes next.

Now, let’s get to the numbers.

We’ll start off with some basics to help you understand who is answering and then get to some more specific experience and equipment prefrences for their home gym.

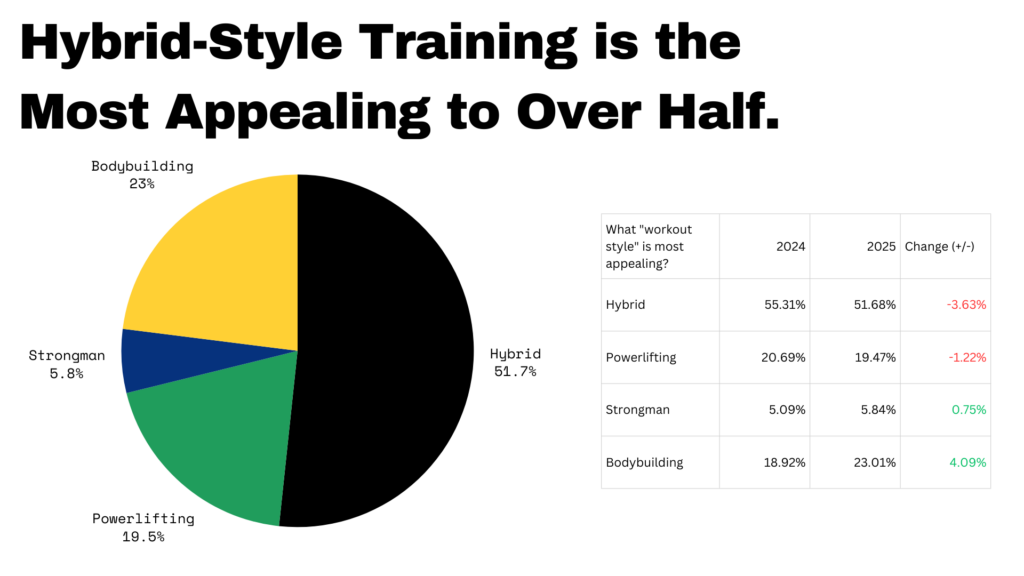

“Hybrid” is the most popular training style.

When compared against niche strength sports like Strongman, Bodybuilding, and Powerlifting, more than half of the respondents describe their training style as “hybrid.” Most people are focused on getting in better shape and aging well — which aligns with the overall vibe I see across the community.

We also saw a noticeable increase in Bodybuilding responses from 2024 to 2025, suggesting that aesthetics are becoming a bigger priority for many lifters.

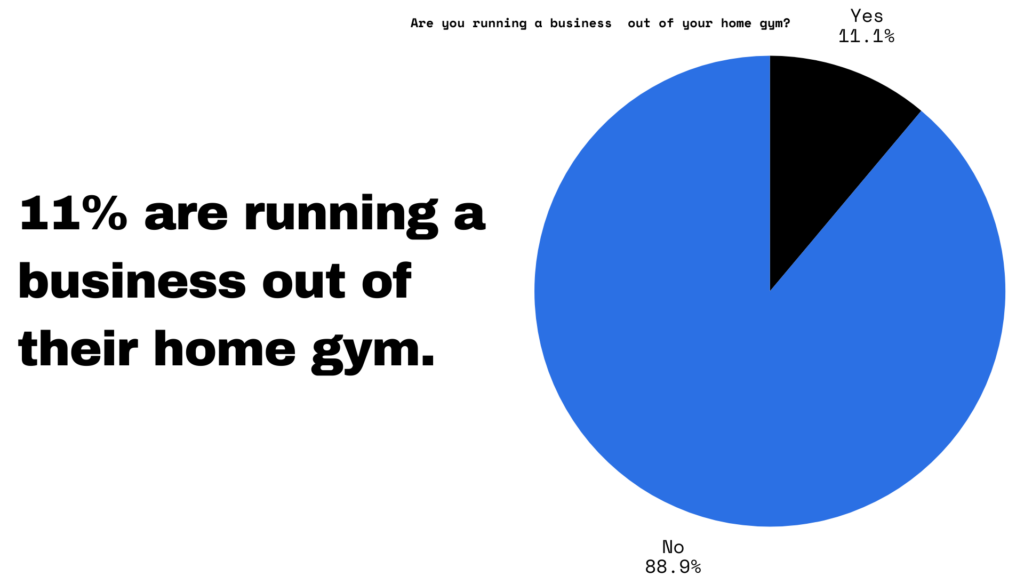

11% are running a business out of their home gym

While 11% may sound small, it likely understates how many people are actually running some form of business out of their home gyms. A large portion of these are personal trainers, but it also reflects a broader trend—home gyms are increasingly becoming income-generating spaces, not just places to work out. For many, the home gym is evolving from a personal expense into a professional asset.

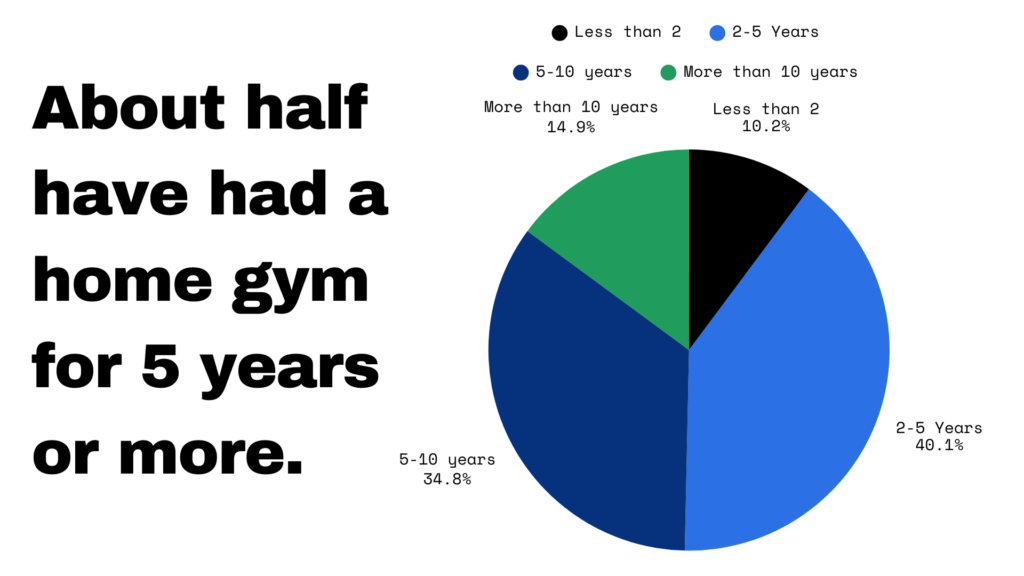

Only a small number have had a home gym for less than 2 years.

Believe it or not, the start of COVID was over five years ago. Many of the people who began their home gym journey during that period are now true “home gym veterans.” While the movement still feels young, the data tells a different story—about half of respondents have owned a home gym for more than five years, and roughly 75% have had one for somewhere between two and ten years. What started as a short-term solution has clearly become a long-term lifestyle.

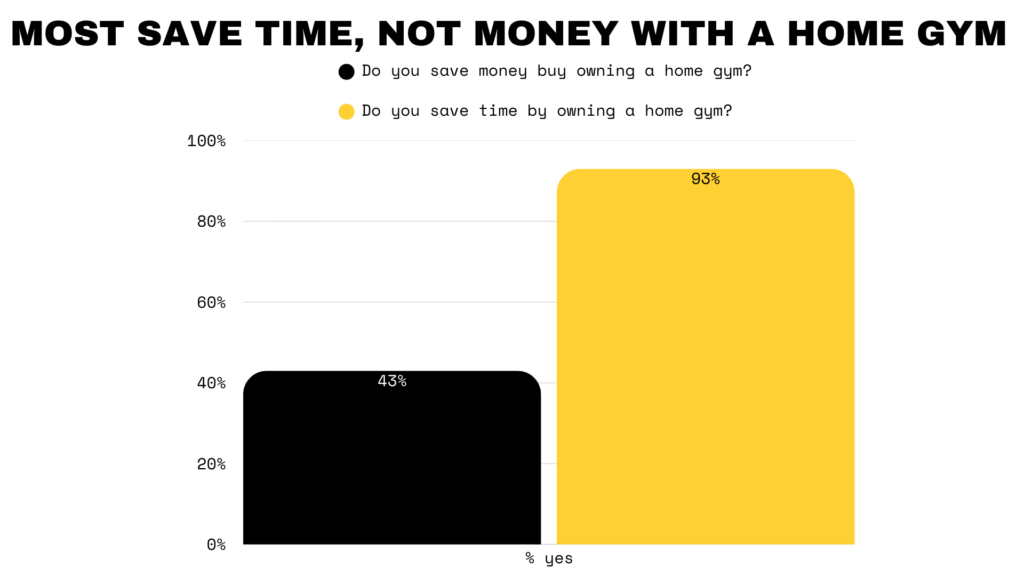

Most save time, not money, from owning a home gym.

43% say they save money by owning a home gym, primarily by removing monthly gym dues, travel expenses, and the hidden costs that come with going somewhere else to train. Over time, those savings add up in a meaningful way.

93% say they save time, making convenience the most overwhelming advantage of training at home. No drive, no waiting for equipment, and no schedule constraints—just the ability to train when it fits, which is ultimately what keeps most people consistent.

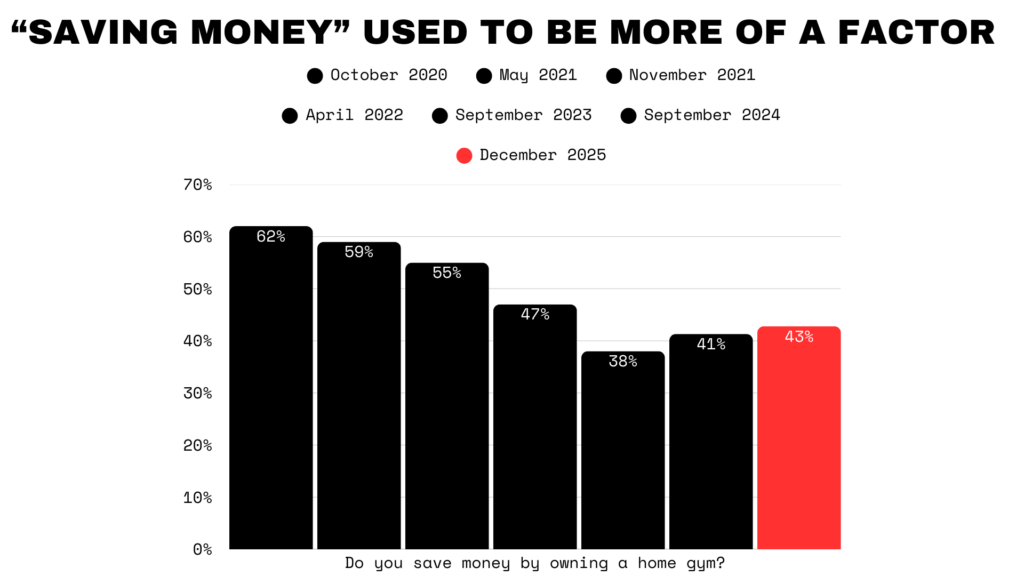

“To save money” used to be a larger factor. Back in October of 2020, about 62% said they saved money by owning a home gym. Most now understand that there are so many more benefits to owning one.

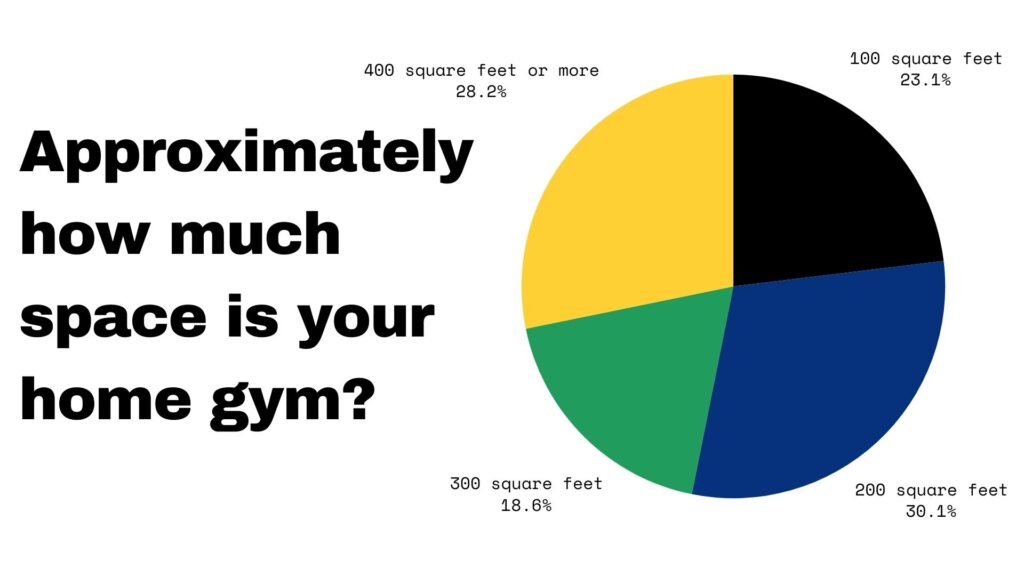

Some home gyms are small, others are larger.

When asked how much space people have for their home gyms, the responses are fairly spread out. The most common answers were around 200 or 400 square feet, but roughly a quarter of respondents are making it work in something closer to a 10×10 space. It’s a good reminder that effective home gyms exist at every scale.

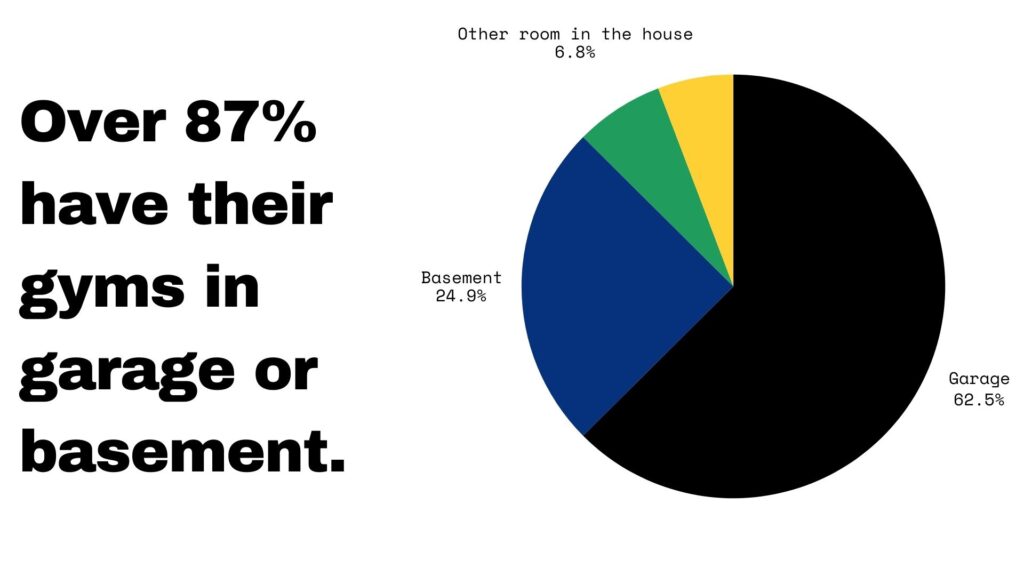

The home gyms are most likely in the garage or basement.

The garage remains the most common home gym location, earning nearly 63% of the votes. Basements come in second at just under a quarter, leaving only a small percentage of people setting up their gym anywhere else.

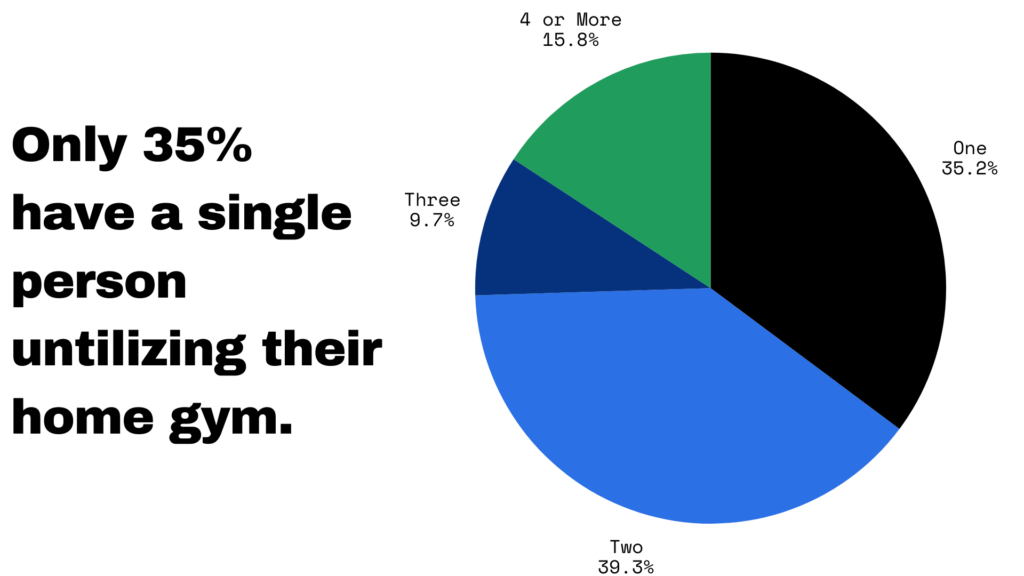

Most have multiple people utilizing their home gym.

When buying equipment, many have to consider who else will be using it, as only 35% have their home gym entirely to themselves. The most common setup is shared between two people, which accounted for 39% of responses.

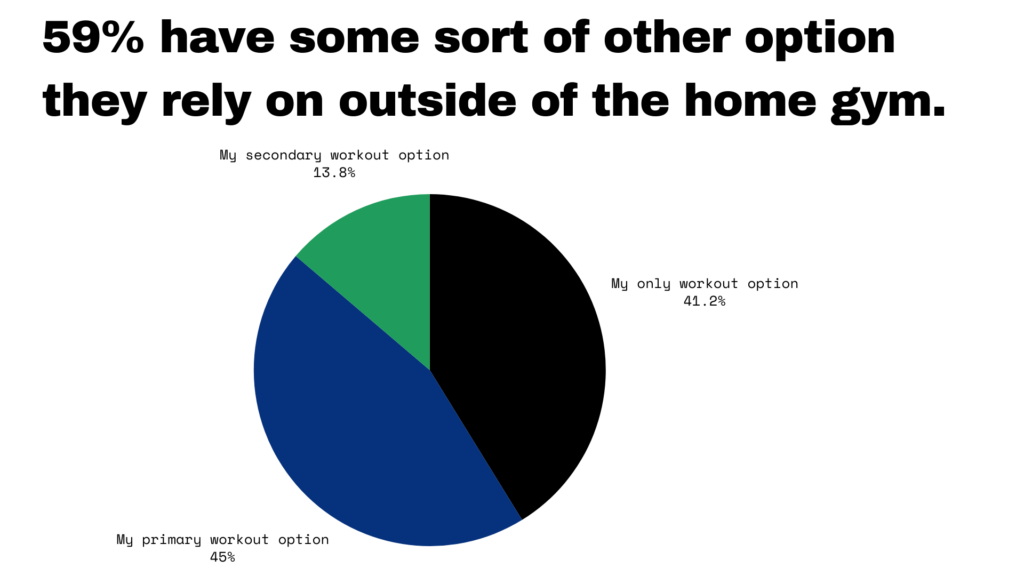

About 60% have some sort of additional workout alternative in addition to the home gym.

While the home gym is the primary workout option for most, only 41% rely on it exclusively as their sole place to train.

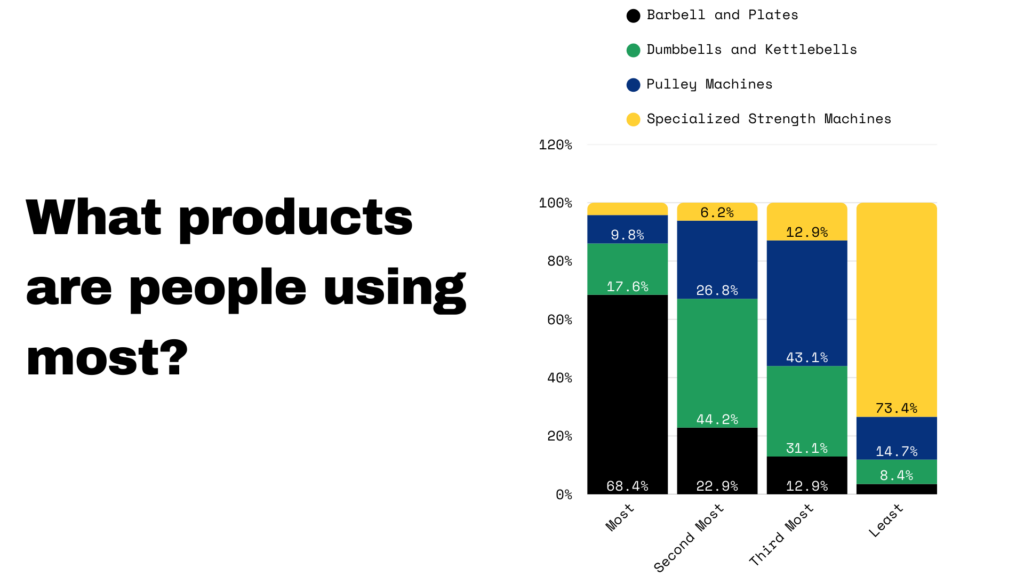

For strength training, barbells and plates are still the #1 item used most often in the home gym.

Barbells and plates dominate as the most-used equipment, earning 69% of the “use most” vote. Dumbbells and kettlebells follow in second, pulley-based machines rank third, and specialized strength machines come in last — though each clearly still has a place in a well-rounded home gym.

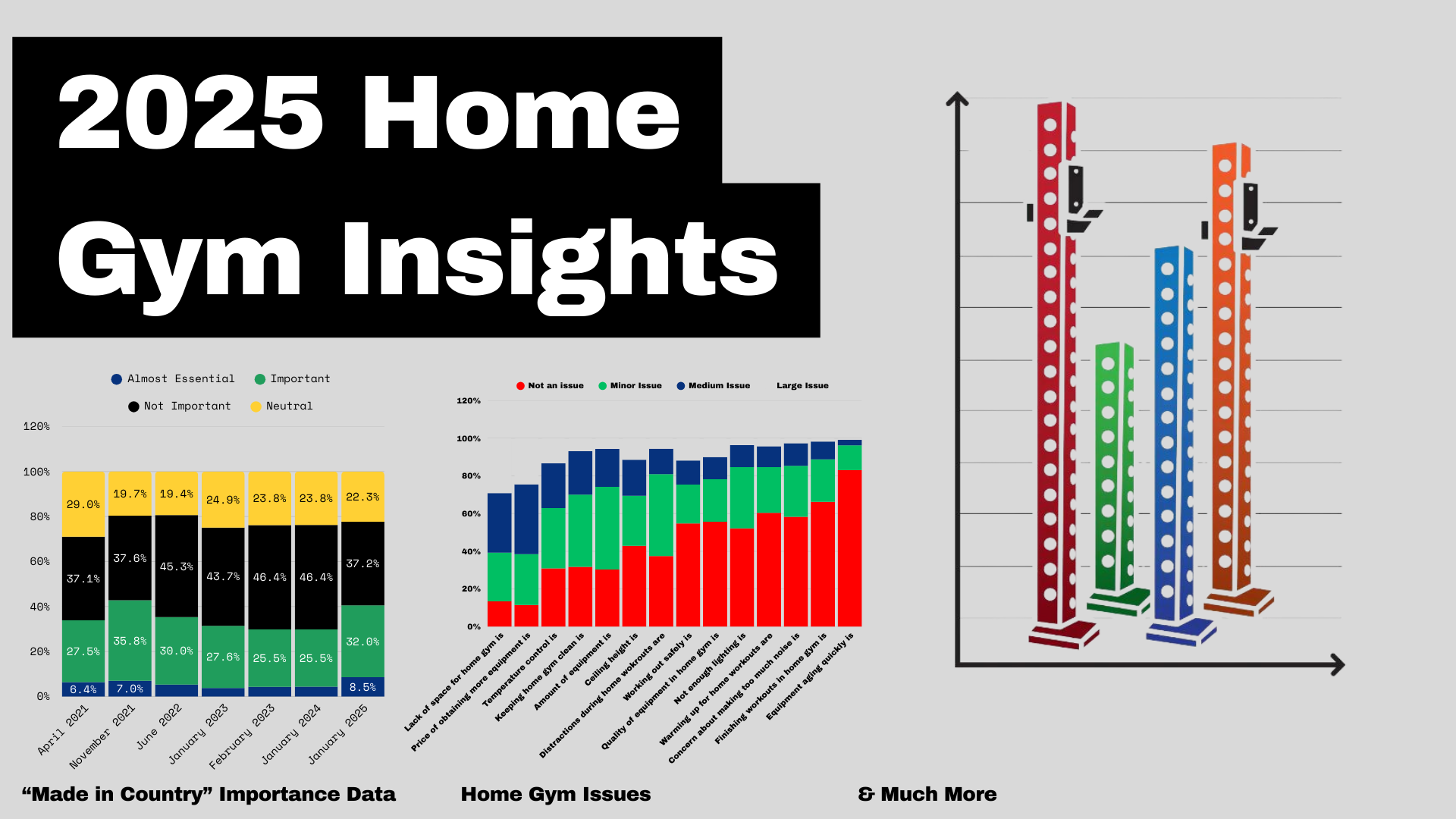

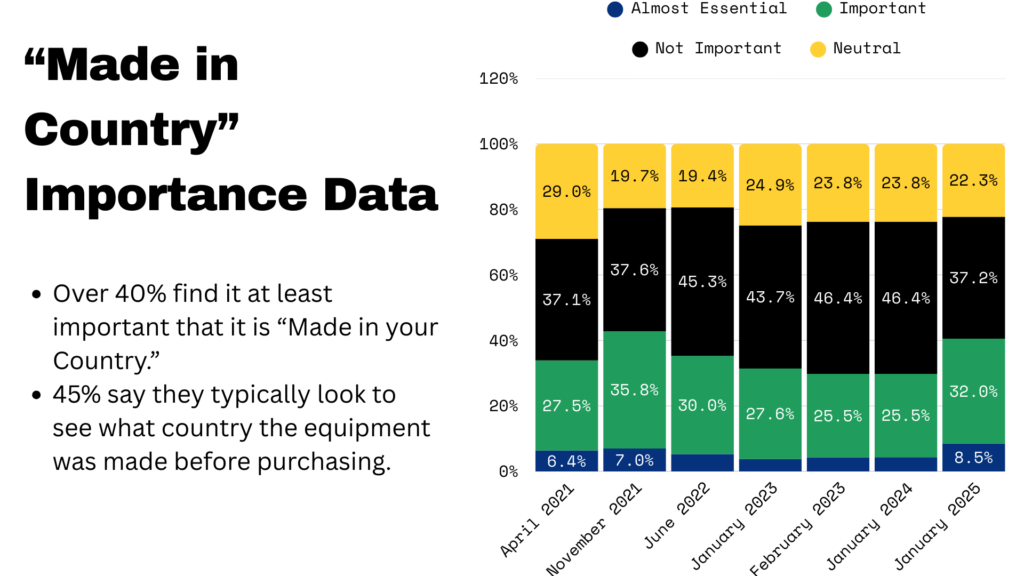

The importance of “Made in your Country” is mixed.

Only about 8.5% said that equipment “made in your country” is almost essential, with another 32% rating it as important. As the chart shows, both figures are up slightly from the year before.

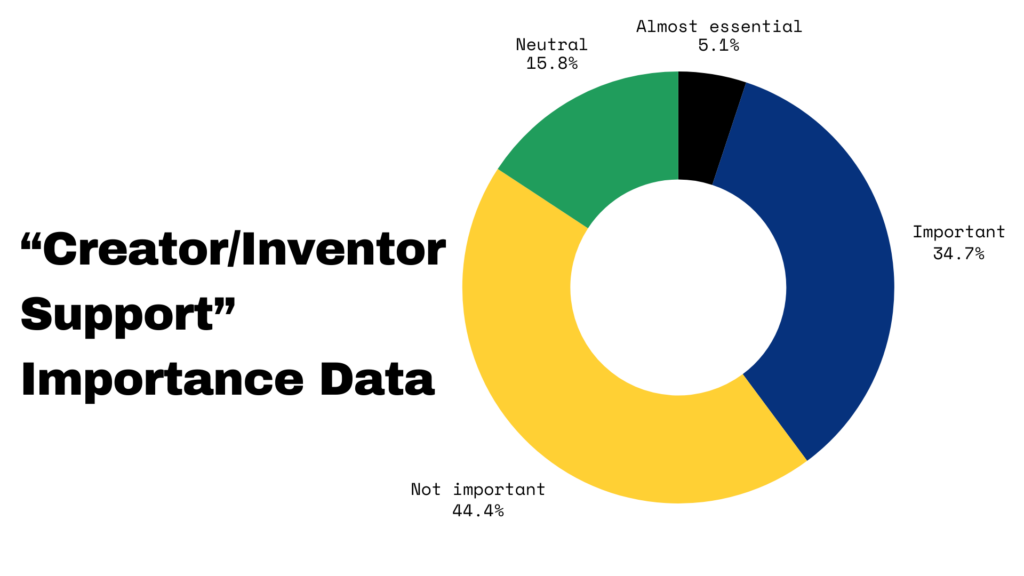

Support of “The Original Creator/Inventor” is at least important to 40%.

Slightly less importance is placed on supporting the “original creator” of a product. About 5% rated this as “almost essential,” while 35% said it is “important.”

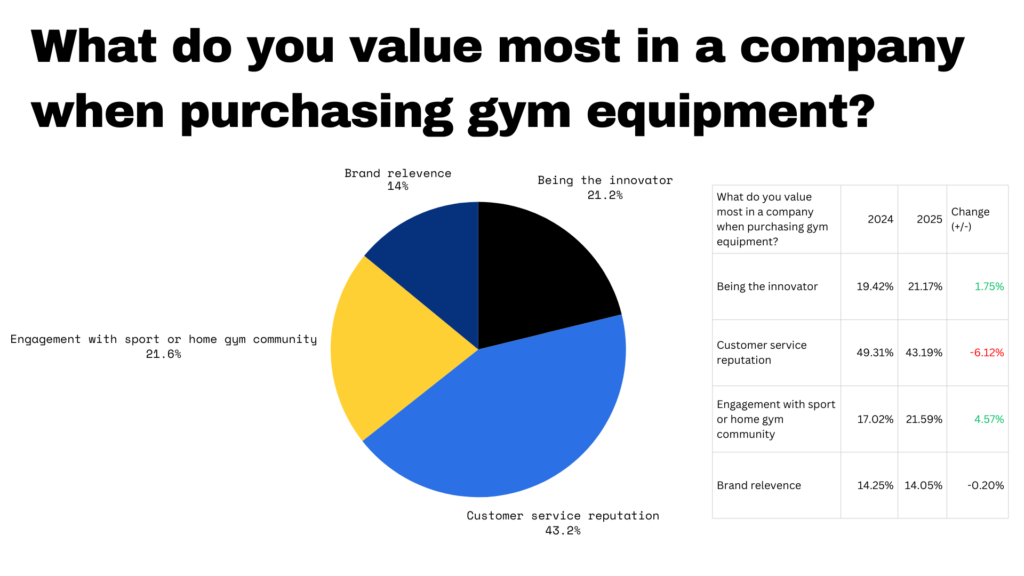

When purchasing gym equipment, Customer Service Reputation is seen as the most important when compared to being the innovator, brand relevance, and engagement with sport or home gym community.

These are business traits that stand out beyond product uniqueness and price. Customer service is the clear leader at 43% of the vote, but we also saw a notable jump in the importance of a brand’s engagement with the sport and home gym community.

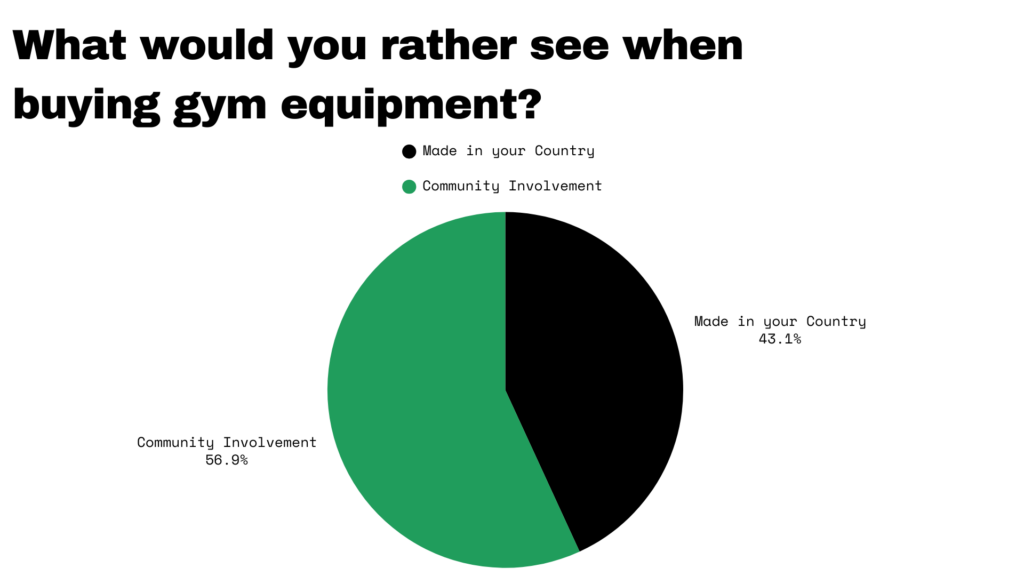

“Community Involvement” is seen as more important than “Made in your Country.”

When asked to choose between the two, about 57% said community involvement matters more than where a product is made.

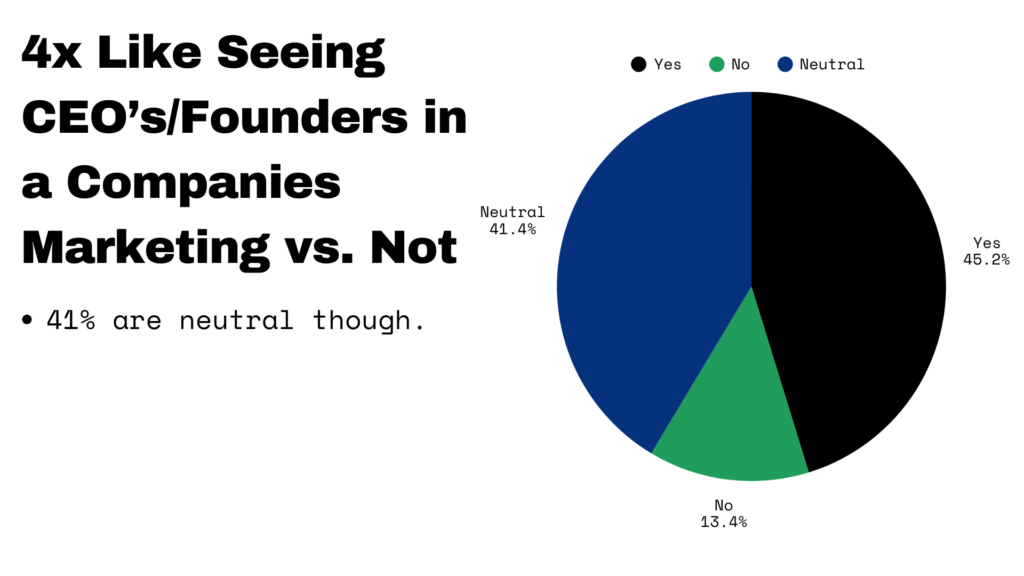

When it comes to seeing founders/CEO’s in marketing, more like to see it vs. not.

Only 13% say that they do not like.

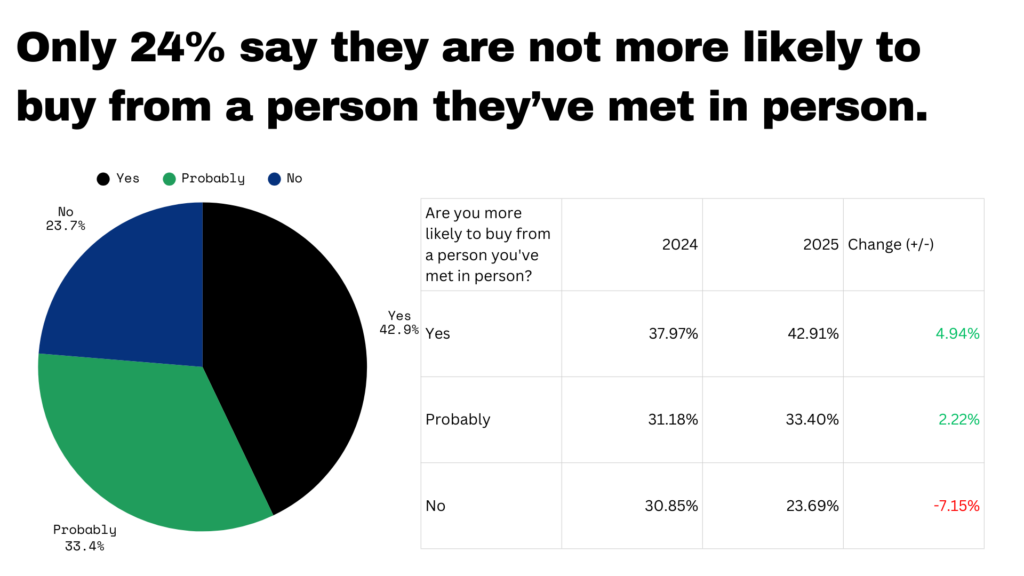

People like to buy from those with whom they have a connection.

When asked if they are more likely to buy from a person rather than a faceless brand, 43% said yes, 33% said “probably,” and 24% said no. Both the “yes” and “probably” responses increased compared to 2024, reinforcing the growing value of personal connection.

PS – HomeGymCon gives brands a direct way to create that connection.

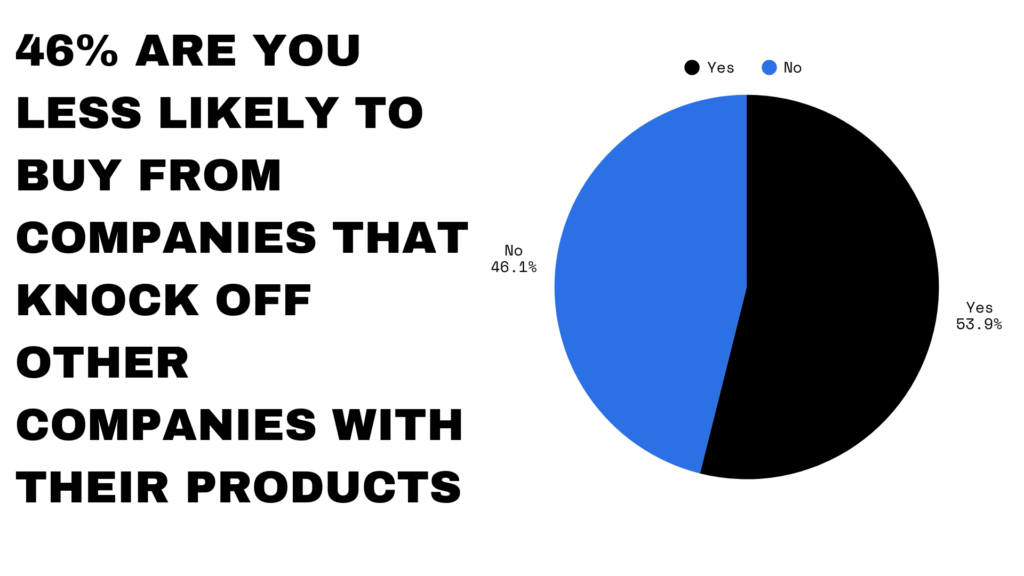

How many care about buying from the knock-offs?

Responses were split on whether people are less likely to buy from a company that knocks off other brands’ products, showing no clear consensus on how much that behavior impacts purchasing decisions.

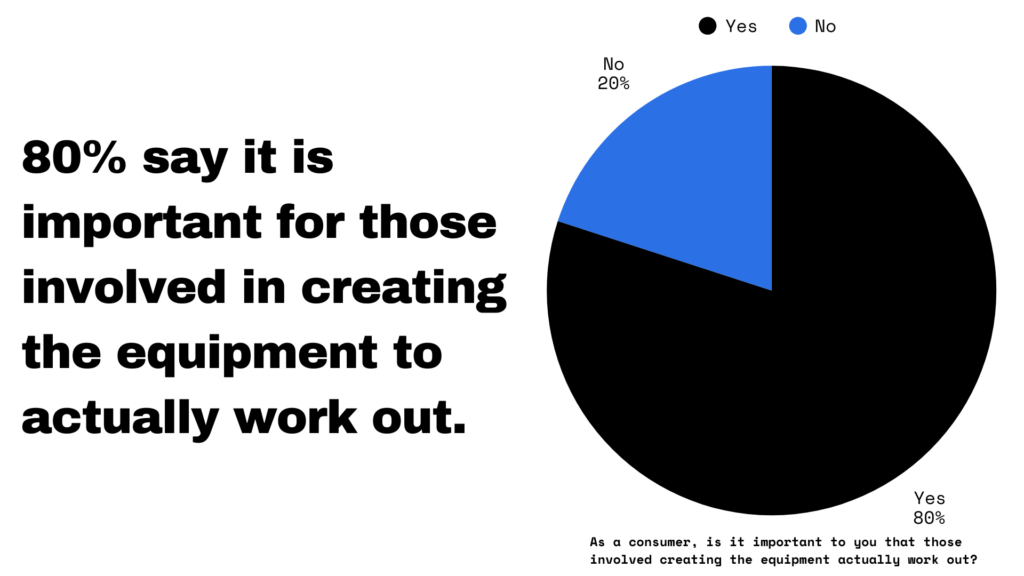

Four out of five respondents believe it’s important that the people creating the equipment actually work out.

Many recognize that products built and refined by those who use them tend to be better than white-label offerings that don’t appear to be iterated on through real-world training.

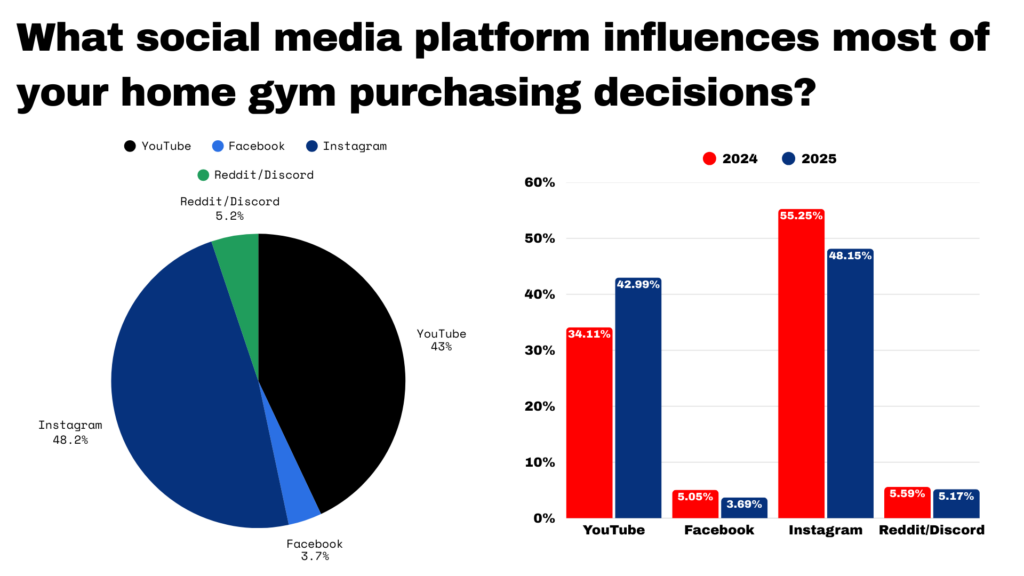

48% say that Instagram is the social media platform that influences most of their home gym decisions.

YouTube is quickly closing the gap. In 2025, 34% selected YouTube, compared to 43% this year. Over that same span, Instagram slipped from 55% to 48%.

Reddit, Discord, and Facebook combined accounted for just about 9% of the vote.

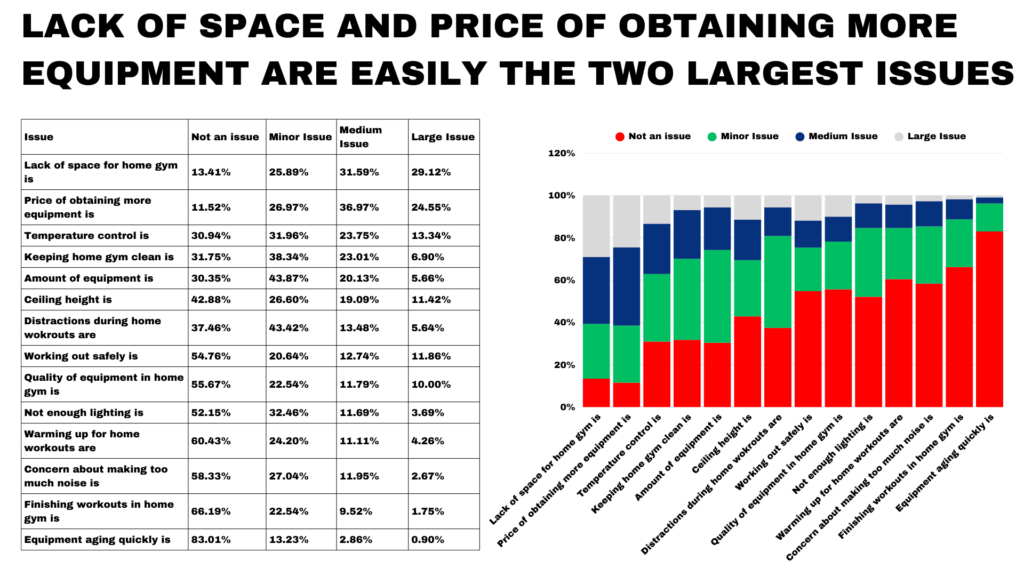

Home Gym Issues

As the numbers show, both lack of space and the cost of adding equipment are at least a “medium issue” for roughly two-thirds of respondents—a significant share. These two clearly stand out as the biggest challenges by far.

That said, there are also several smaller and mid-level pain points with much more room to be solved. You can take a deeper look at the numbers here – 2025 home gym issues.

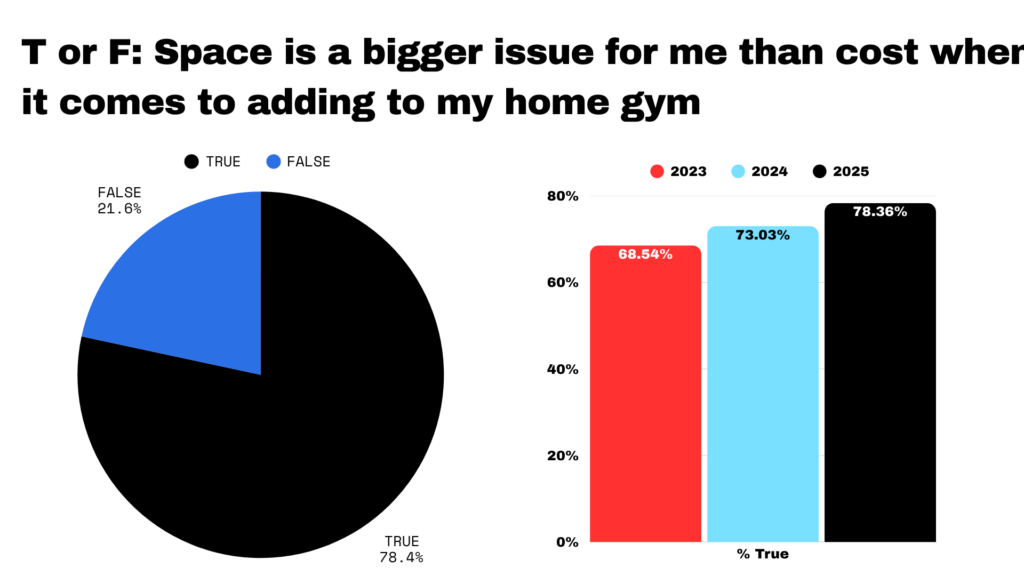

While lack of space and the price of equipment seem extremely close in the chart above, when put up head to head, nearly 4 out of 5 say that space is a larger issue than the cost of new equipment.

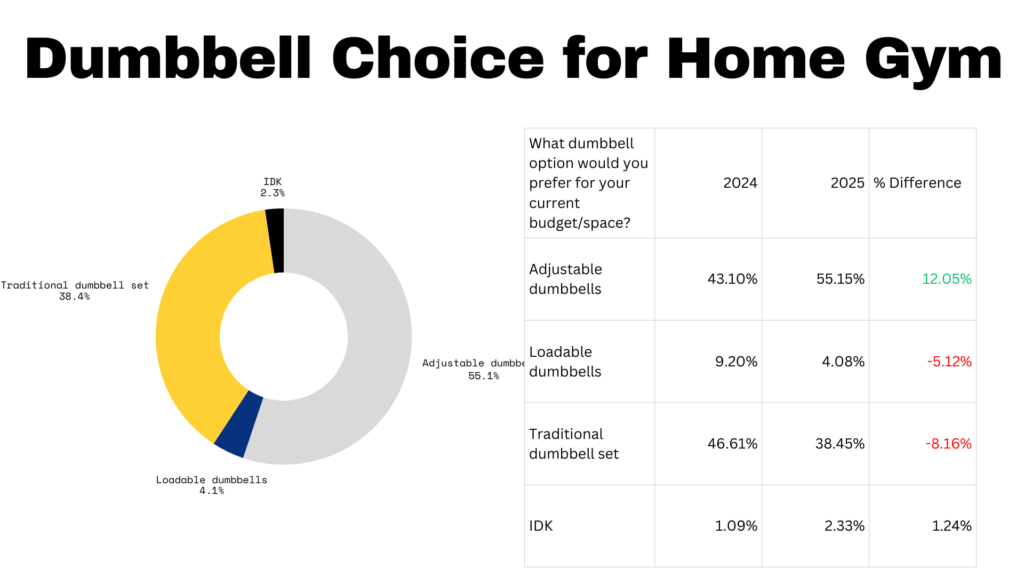

Adjustable Dumbbells have surpassed the popularity of traditional dumbbell sets.

As adjustable dumbbells continue to improve, they’ve overtaken traditional sets as the top choice. About 55% prefer adjustable, compared to 38% for traditional dumbbells and just 4% for loadable options.

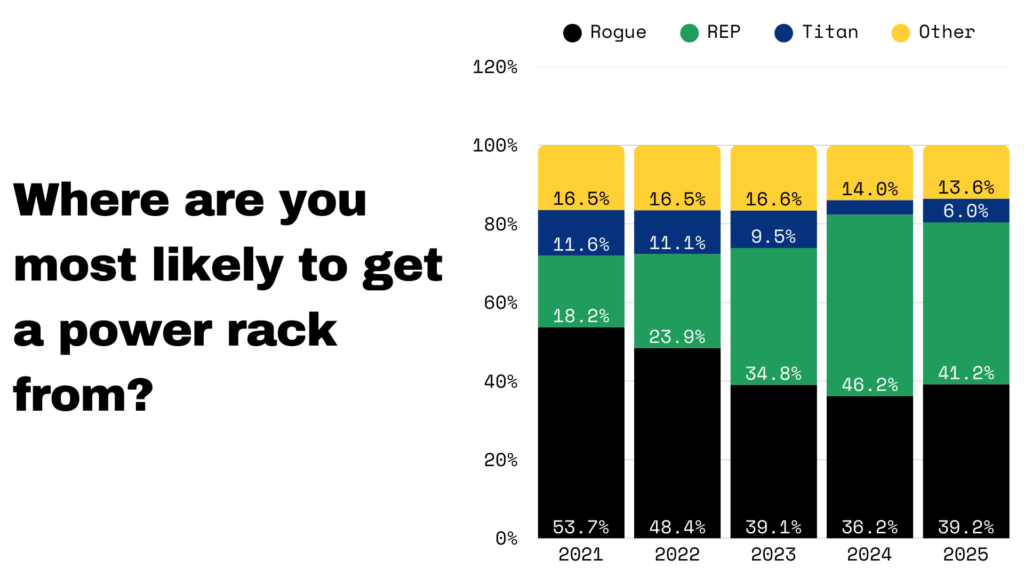

REP still the top “rack choice”

When comparing Rogue, REP, Titan, and others, 41% chose REP and 39% chose Rogue, with Titan and all other brands combining for roughly 20% of the vote.

This is a question we’ve asked since 2021, and it clearly shows how REP closed the gap with Rogue in just a few years. That said, Rogue did regain a bit of ground this past year.

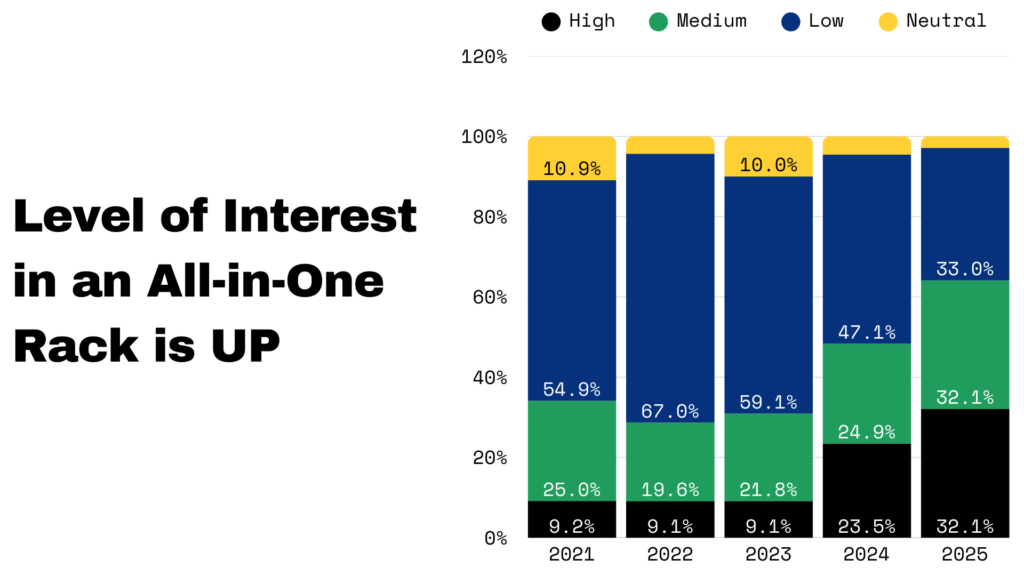

All-in-One Racks are gaining interest quickly

In 2025, 32% expressed high interest in all-in-one racks. That compares to just 9% from 2021–2023 and 23.5% in 2024. As these systems continue to improve, more people are seeing them as a worthwhile investment.

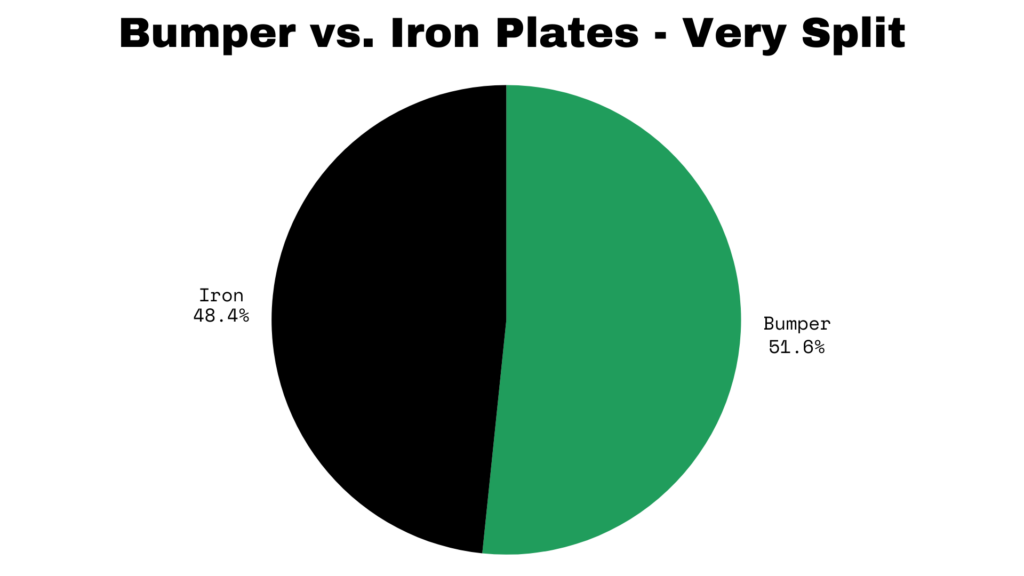

Bumper plates vs. Iron plates – pretty close to 50/50.

Bumper plates narrowly edged out the win, but the split is tighter than in past years, when bumpers typically hovered around 60% of the vote.

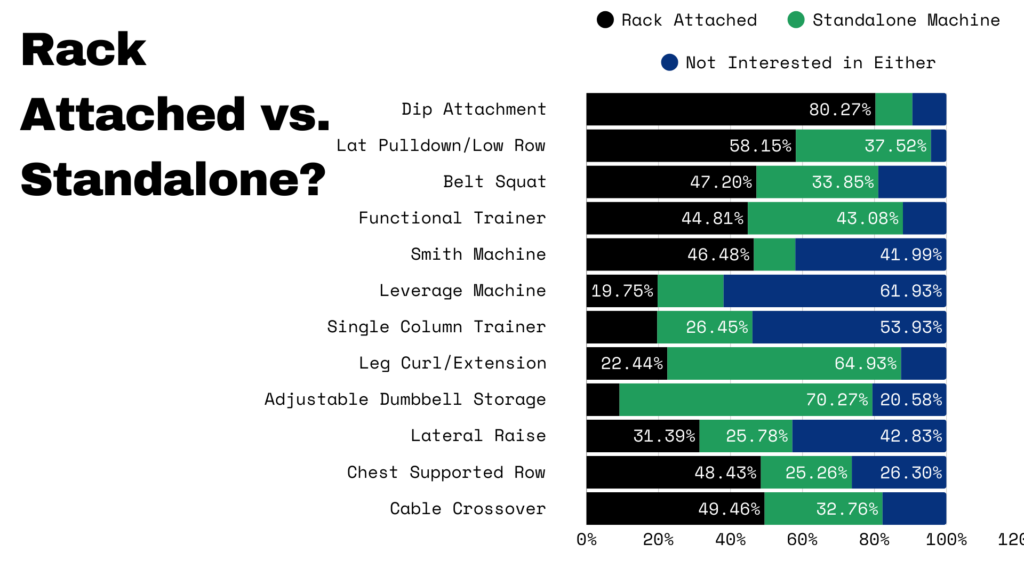

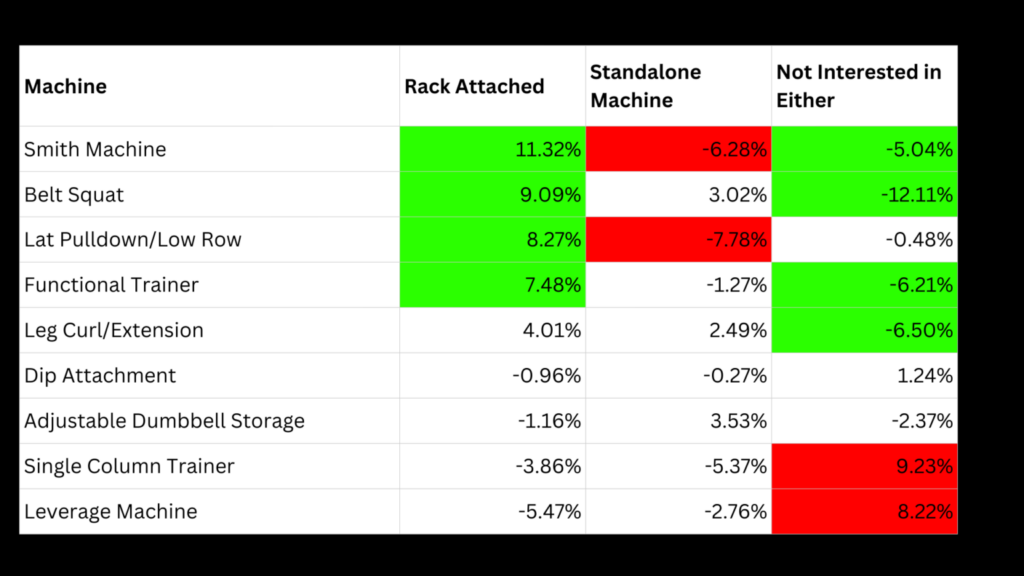

Rack Attached or Standalone?

Below are several potential rack-attached options and standalone machines for a home gym, sorted from the highest to lowest percentage of rack-attached votes.

As the chart shows, there is strong demand for rack-attached lat pulldowns, belt squats, functional trainers, and Smith machines. Take a deeper look here.

You’ll also see the year-over-year change. Smith machines, belt squats, lat pulldown/low-row units, and functional trainers all saw a meaningful increase in rack-attached votes compared to last year.

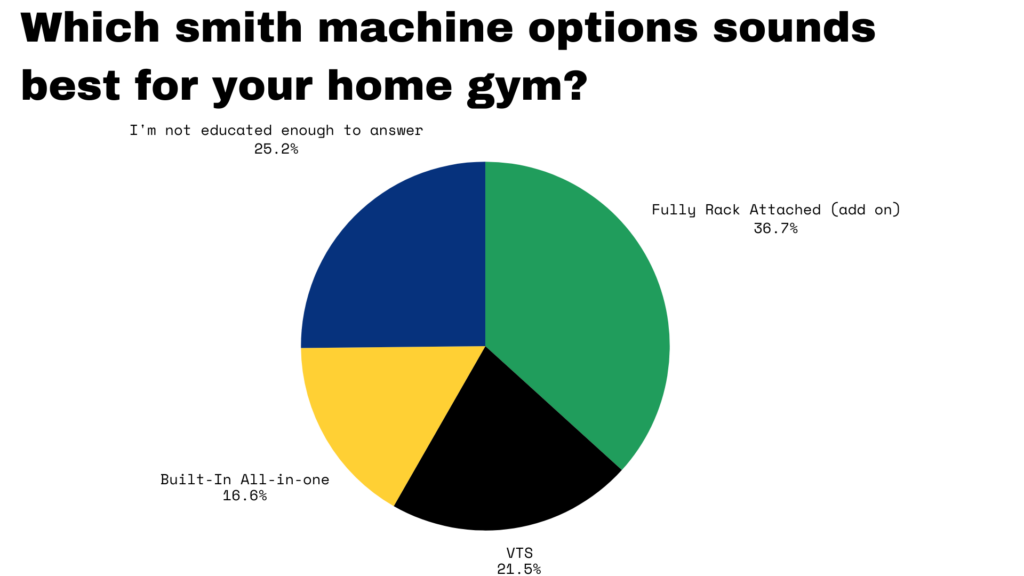

The fully rack-attached Smith machine option tops the VTS and is built-in all-in-one.

We’ve seen a number of rack-based Smith machine options released or updated over the past few years. While the votes are fairly spread out overall, the fully rack-attached design was the most popular choice. About a quarter of respondents also said they weren’t educated enough on the options to answer.

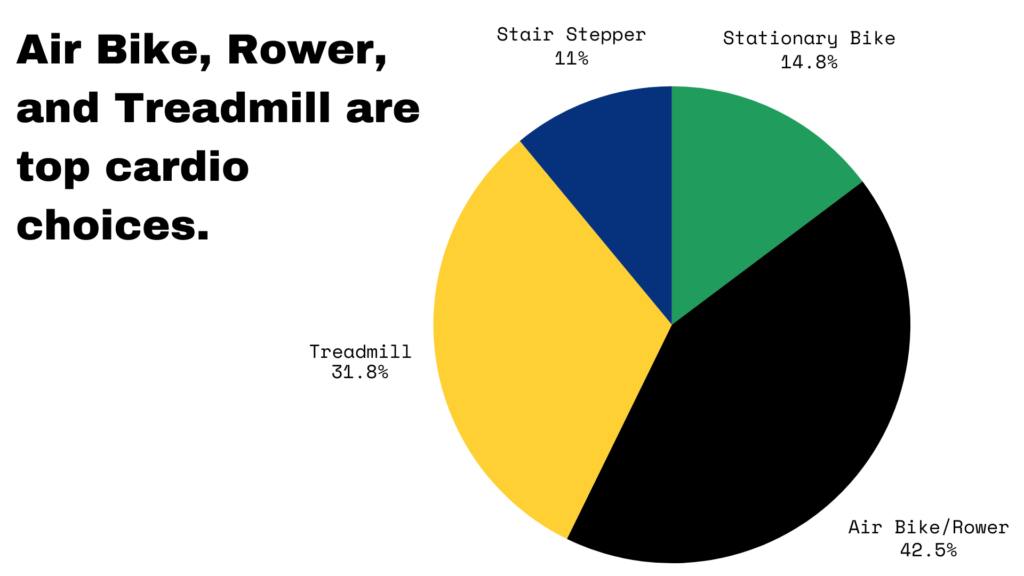

Air Bike/Rower/Treadmill are the top cardio options among this group of respondents.

This is one of the questions where I wish we had more than four options (an Instagram limitation). That said, the treadmill is likely the top choice for most, with air bikes and rowers grouped together into a single option.

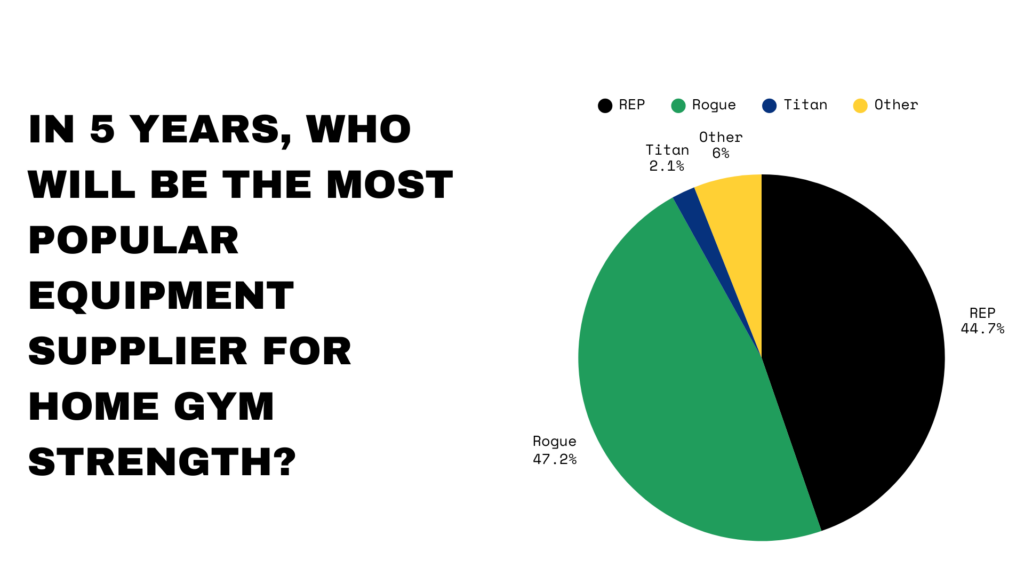

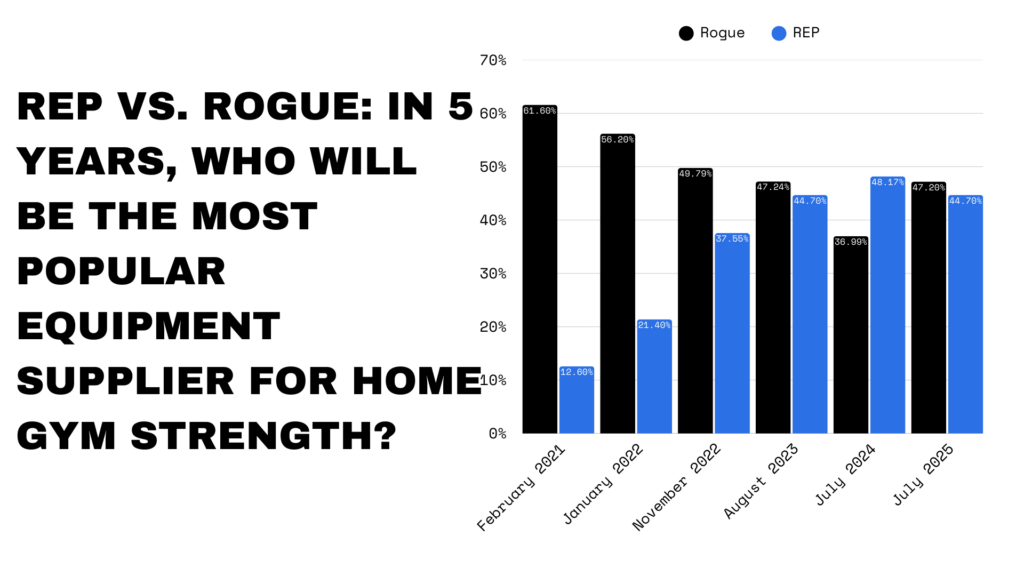

Most believe that Rogue or REP will be the most popular equipment supplier for home gym strength in 5 years.

They received over 91% of the votes. Only 6% voted “other.”

Over the past five years, REP steadily chipped away at Rogue’s lead and even overtook them in 2024. While the race remains tight, Rogue reclaimed the top spot in 2025 for this question.

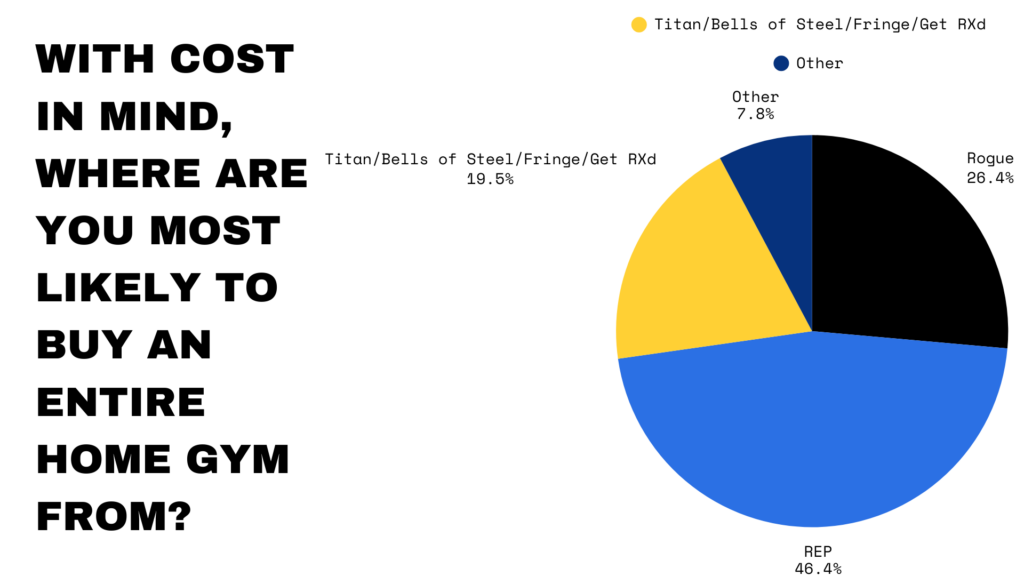

With cost in mind (and you had to choose a single company), about 46% would choose REP with cost in mind.

This likely reflects the reputation REP has built around balancing quality with affordability over the years.

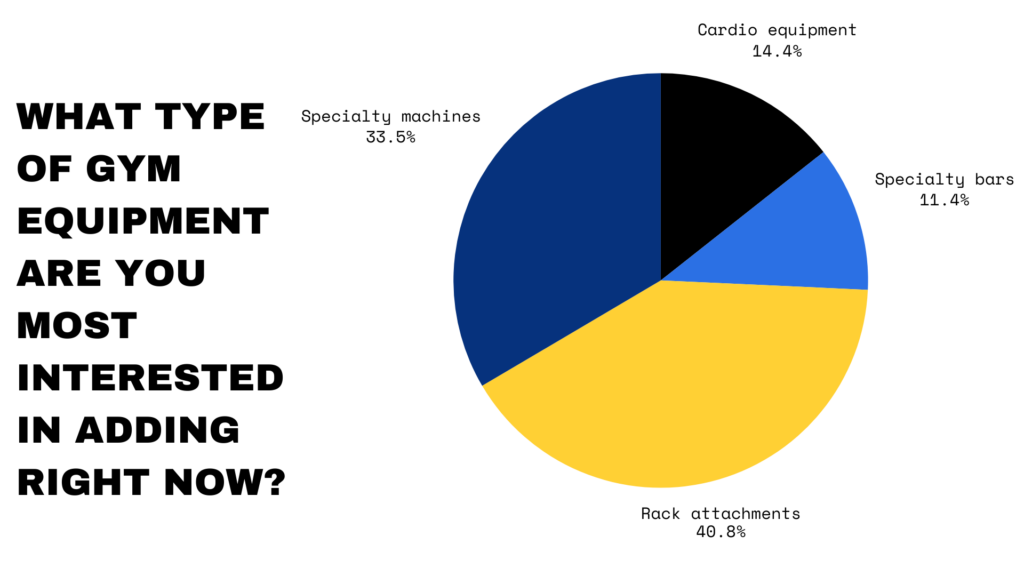

Rack attachments narrowly edged out specialty machines as the type of equipment most people are interested in adding right now.

Together, these two categories accounted for roughly three-quarters of the votes, well ahead of cardio equipment and specialty bars.

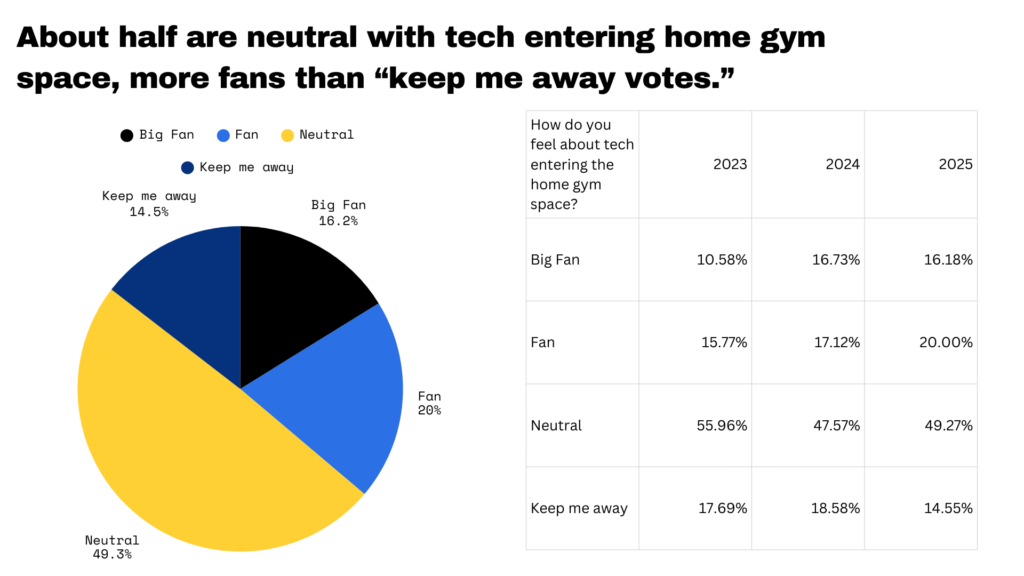

Interest in Tech invading home gyms is mostly neutral.

What stands out here is that the ceiling is much higher than the floor is low. Only 15% are truly against tech in the home gym, while 85% are either open to it or already fans. Nearly half sit in that neutral middle, which tells me this isn’t about rejection—it’s about trust and usefulness. If technology actually makes training better, saves space, or simplifies the experience, there’s a massive group that could be converted. The opportunity isn’t convincing skeptics; it’s proving value to everyone who’s still on the fence.

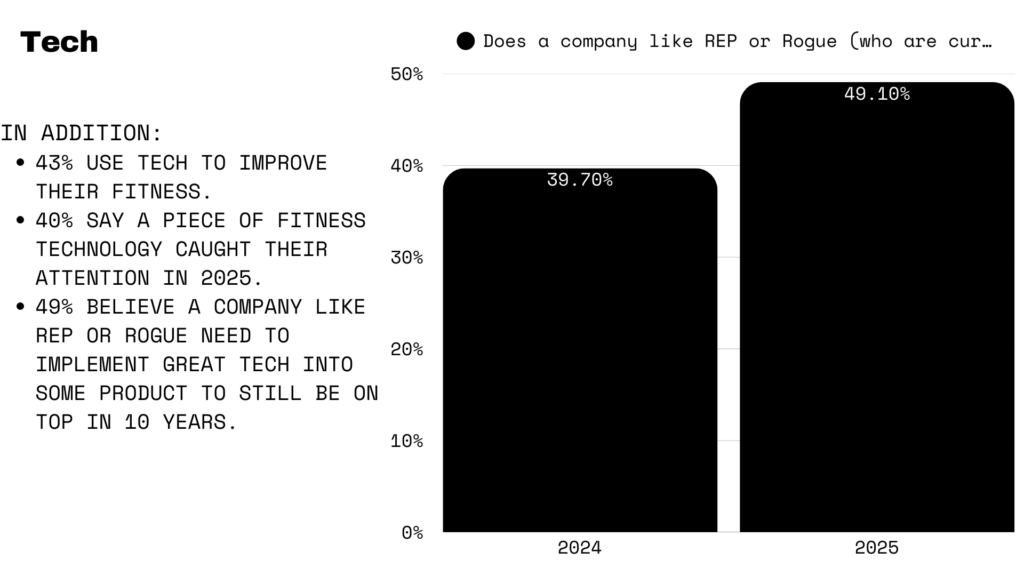

Below are some additional stats about tech in the home gym space:

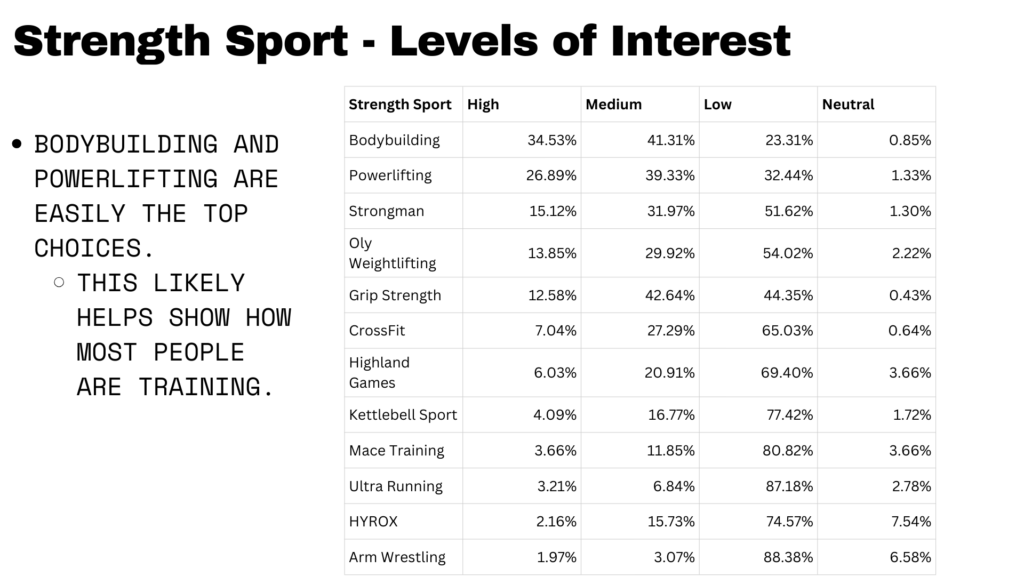

The Levels of Interests in Specific Strength Sports

The results show a wide range of interest levels, highlighting that all of these are relatively niche sports within the home gym community. Bodybuilding and powerlifting stand out as the clear leaders, drawing the strongest engagement overall. Strongman, Olympic weightlifting, and grip strength also show solid followings, each with over 40% of respondents expressing high or medium interest.

In addition, about 31% say they train for a specific strength sport.

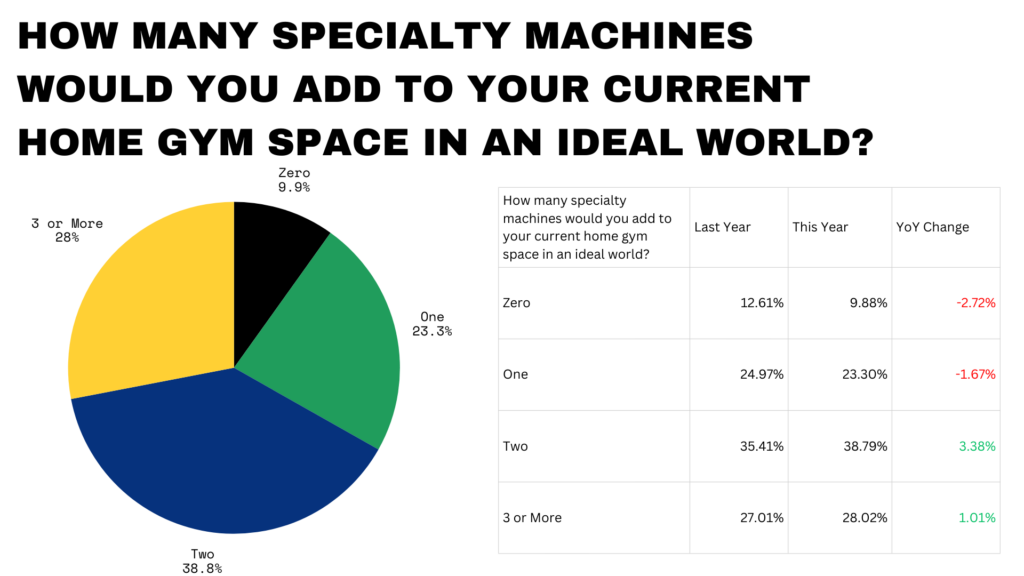

Very few say they would not like to have any specialty machines within their current home gym space.

In fact, more than two-thirds say they would like to have at least two. Interest in adding specialty machines to home gyms is also up slightly from last year, signaling a continued shift from “bare essentials” setups toward more complete, purpose-built training spaces.

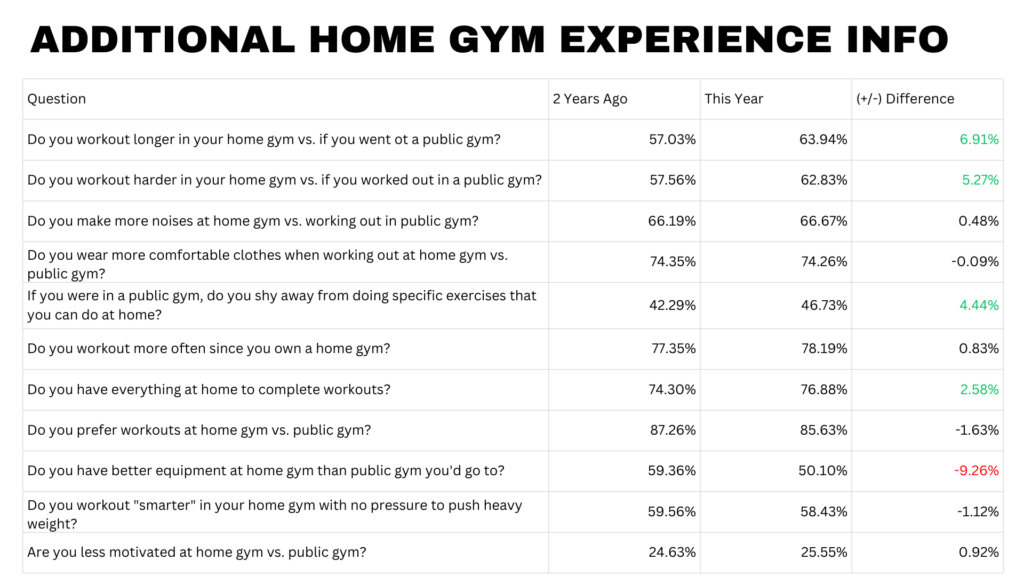

Most Enjoy their Home Gym Workout Experience

Below are several questions about your home gym workout experience and how it compares to last year.

Overall, the results show that most people who train at home really enjoy the lifestyle.

A few that stand out include:

- 64% say they work out longer in a home gym vs. a public gym.

- 63% workout harder in the home gym vs. the public gym.

- 78% of people work out more often because they own a home gym.

- 86% prefer home gym workouts to public gyms.

- Only 26% say they are less motivated at a home gym vs. a public gym.

Conclusion

The biggest takeaway from these results is that the home gym isn’t a “new trend” anymore — it’s a long-term lifestyle. A large portion of respondents have been training at home for years, and many who started during the early COVID wave are now true home gym veterans. This group isn’t experimenting anymore; they’ve built habits, learned what works in their space, and are continuing to upgrade their setups over time.

Convenience remains the clearest driver. Saving time is nearly universal, and that advantage shows up everywhere else: people train more often, work out harder, spend longer in the gym, and overwhelmingly prefer home workouts to public gyms. At the same time, space is still the biggest constraint for most, which is why we continue to see growing interest in rack attachments, all-in-one systems, and equipment that adds versatility without adding a large footprint.

Finally, purchasing decisions are becoming more relationship-driven than ever. Customer service, community involvement, and personal connection consistently rank high — often above factors like where a product is made. People want to buy from brands they trust, from founders they can see, and from companies that actually use what they build. Overall, the direction is clear: home gyms are getting more dialed-in, more intentional, and more complete — and the brands that win will be the ones that solve real space and training problems while building real trust with the community.